New Delhi15 minutes ago

- copy link

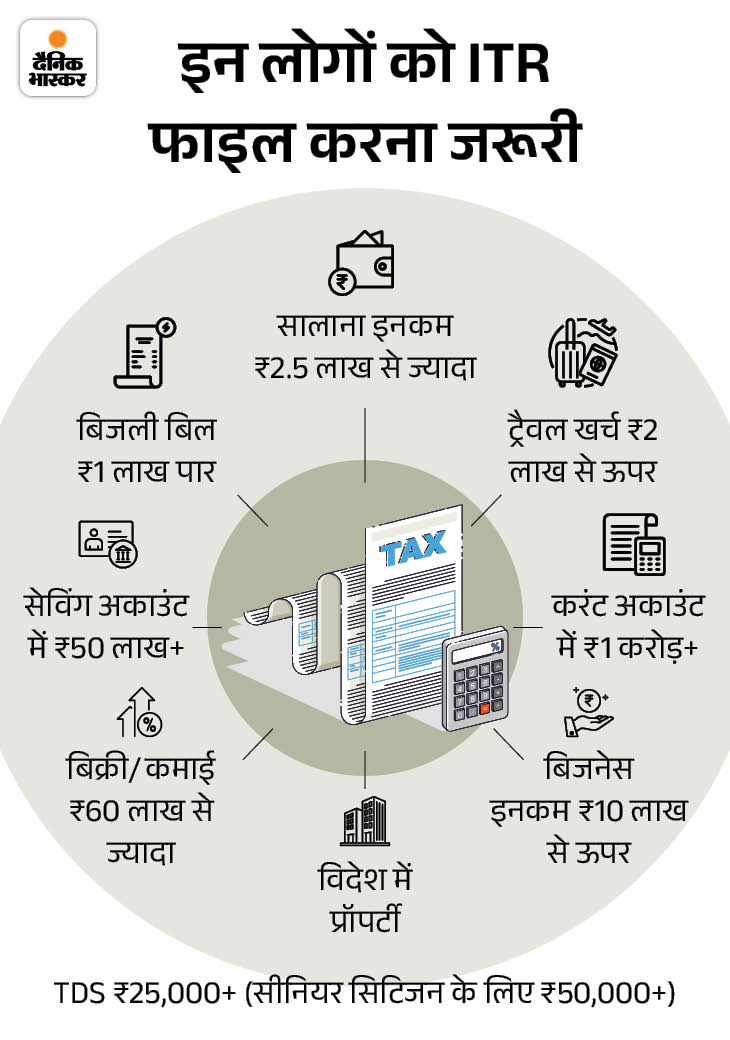

Income tax return i.e. ITR filing for the financial year 2025-26 has started. The last date for filing returns for general taxpayers is July 31, 2026. Whereas for some people of business class (ITR-3 and 4) it is 31st August.

If you miss the deadline by July 31, you can file a ‘belated return’ by paying the penalty by December 31. ITR is the official record of your entire income, investments and financial transactions.

The Income Tax Department collects information on bank accounts, TDS, share-mutual funds, property and foreign travel through AI, data analytics and various portals and matches it with the information given in the ITR.

In such a situation, even a small mistake can lead to tax demand, interest and penalty. Here Tax Expert and CA Anand Jain, Indore We are telling you which 10 important things should be kept in mind while filling ITR…

1. Don’t rely only on Form 16

Many salaried people think that whatever is there in Form 16 is enough. But Form 16 only gives information about salary and TDS deducted on it. If you have received FD, RD, savings account interest, dividend, rent, freelance income, share-mutual fund profit or foreign income, then it is important to include it in ITR. Hiding these may result in paying additional tax and interest later.

2. It is very important to choose the right ITR form

If you choose the wrong form, the return may be considered defective, that is, it will be considered that you did not file the return at all.

- ITR-1: For salary, pension and simple interest income earners.

- ITR-2: For those with capital gains, more than one house, foreign assets or income.

- ITR-3: For those doing business, freelance, F&O or trading.

- ITR-4: For small businessmen and professionals.

3. Must check AIS, TIS and Form 26AS

Before filing the return, please match Form 16, Form 26AS, Annual Information Statement (AIS) and Taxpayer Information Summary (TIS). If the income shown in these is different from your return, the department may seek clarification. If you see incorrect information, file a complaint for correction on the portal.

4. Add the salaries of both the companies when you change jobs.

If you have changed job in the financial year, then file the return by adding the salary received from both the old and new employer. If you do not do this, you may have to pay tax later due to less TDS being deducted.

5. Fill the bank account details correctly

Provide information about all bank accounts. Enter the correct IFSC code and account number of the account where the refund is coming. Mistakes may delay refunds.

6. Don’t make the mistake of hiding interest income

Many people think that if TDS is not deducted then the income is not taxable. This is wrong. The department gets to know the interest of FD, RD, savings account and bonds from AIS and bank data. Leaving them can be costly.

7. Give complete details of sale of shares, mutual funds and property

Since the demat account is linked to PAN, all transactions come to the department. Declare both profit and loss on sale of shares, redemption of MF or sale of property. Showing losses can lead to tax savings in future.

8. Claim deductions with documents

Take deductions like 80C, NPS, 80D (Health Insurance) and interest on home loan only on the right investments. Keep the documents safe, the department can ask for proof anytime.

9. Full disclosure of foreign investments and income

Those investing in foreign shares, ETFs, bank accounts or platforms are required to provide details. Especially for Residency and Ordinary Residency tax payers, it may be necessary to provide information about foreign assets.

10. Do e-verification after filing returns

Submitting returns is not enough. It is necessary to do e-verification through Aadhaar OTP, Net Banking, Demat Account or Digital Signature. If not done on time, the return may be invalid.

July 31st is the last date, if there is delay then fine will be imposed

Source link

[ad_3]