New Delhi48 minutes ago

- Copy link

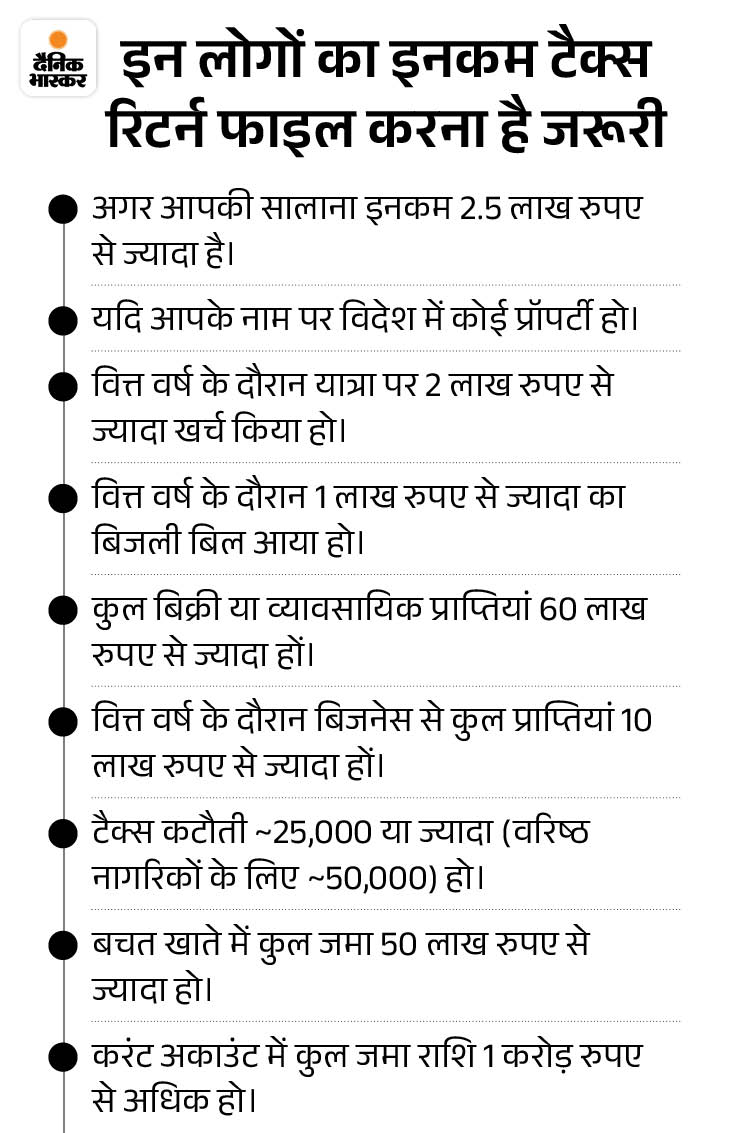

There is less than 1 month left for income tax return fine (ITR) for FY 2024-25. This time, 15 September last date has been kept for this. In such a situation, if you have not yet filed ITR, then do it as soon as possible. Otherwise you may have to face many problems.

According to Tax Expert Chartered Accountant (CA) Anand Jain (Indore), filing ITR in time not only protects against penalty, but also has 4 more benefits.

First of all, know what is the Income Tax Return (ITR)? Income tax return (ITR) is a kind of account that you give to the government. In this, you tell you how much earning you have earned last year, what earnings have to be paid and how much tax you have paid in advance. This shows that as tax, you will give some more money to the government or the government will return some money to you.

1. You will avoid fine If you do not file ITR within the stipulated date, you may have to pay a penalty. If the annual income of an individual taxpayer is more than Rs 5 lakh, then it will have to pay a late fee of Rs 5,000. If the annual earning of the taxpayer is less than Rs 5 lakh, then it will have to pay Rs 1,000 as late fees. This fine can be avoided by filing ITR on time.

2. There will be no fear of notice Right now your income information from many sources gets the Income Tax Department, the Income Tax Department can send you notice on the basis of those information if ITR is not filled on time. It is beneficial to deposit ITR on time to avoid the problems of notice.

3. Savings of interest According to the Income Tax rules, if a taxpayer has not paid the tax or has repaid less than 90% of the total tax made on it, then it will have to pay 1% interest penalty every month under Section 234B. In this way, you can save interest on income tax by filing returns from time to time.

4. Carrie will be able to forward the loss According to the Income Tax rules, you can forward your loss for further finance years by filing ITR till the scheduled date. That is, in the next financial years you can reduce tax liability on your earnings.

For example, if there is a loss on the sale of shares, then it can be forwarded for 8 years. However, if the return file is not gone on time, then the loss cannot be carried and this benefit will not be available.

Source link

[ad_3]