Last Updated:

India sources 80% of its ammonia needs from the Gulf region and that supply is now at a standstill

![]()

Workers load sacks of fertiliser in Amritsar, India, in 2025. (Image Courtesy: Narinder Nanu/AFP via Getty Images)

Since the United States and Israel launched strikes on Iran on February 28, the Strait of Hormuz has been nearly entirely closed to non-Iranian shipping. The strait is 21 miles wide at its narrowest point, and India, one of the world’s largest fertiliser consumers, is already absorbing the damage with its monthly urea production having dropped by 8,00,000 tonnes out of its normal 2.6 million. LNG flows from the Gulf dried up, and ammonia imports followed. India sources 80% of its ammonia needs from the Gulf region and that supply is now at a standstill.

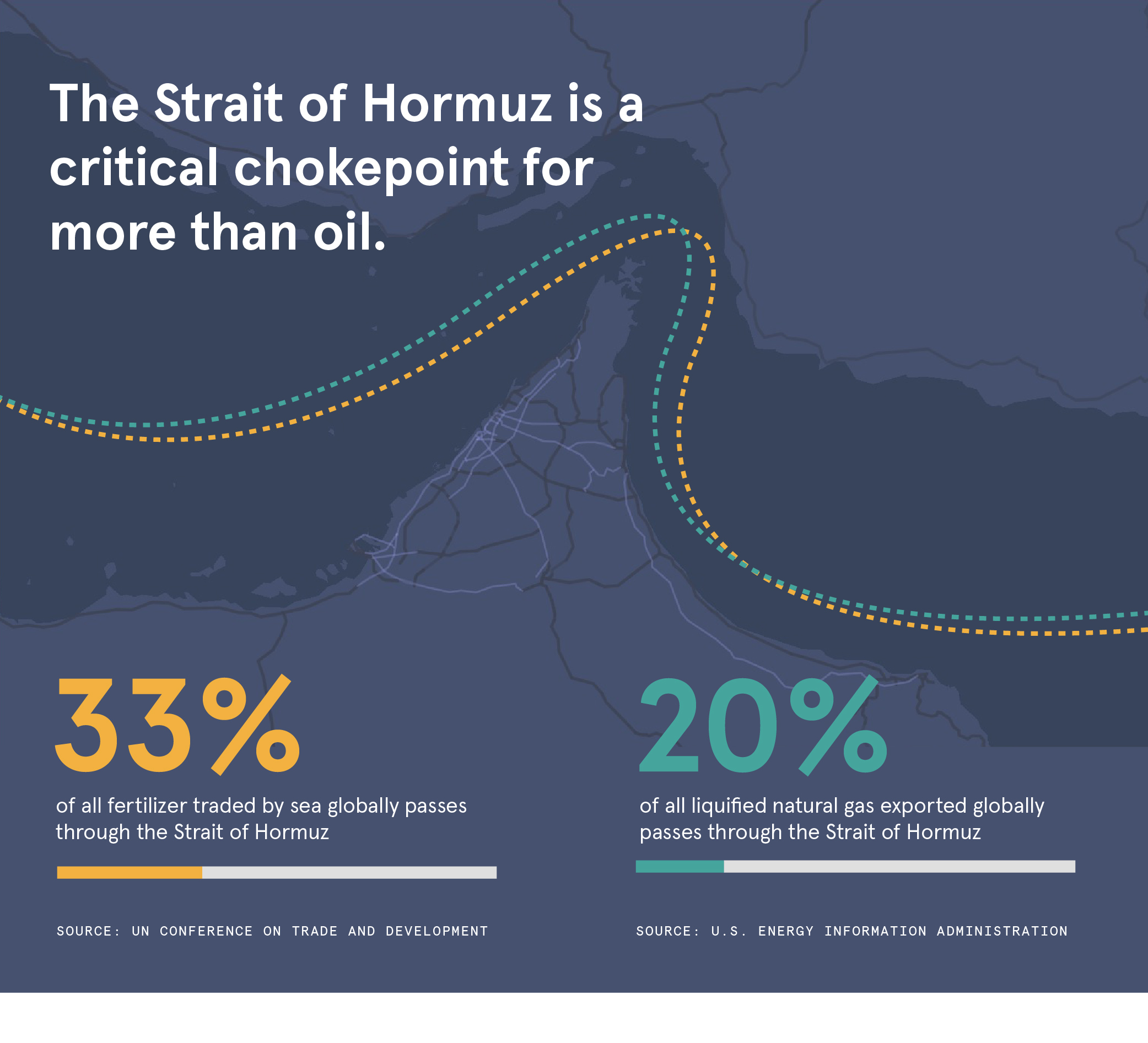

A Narrow Strait, A Very Wide Problem

The Strait of Hormuz has always carried more than oil. The Gulf states (Saudi Arabia, Qatar, the UAE, Iran, and Bahrain) account for 49% of globally traded urea and 30% of globally traded ammonia, both nitrogen-cycle inputs without which modern, high-yield agriculture cannot function. One-third of all seaborne fertiliser trade moves through this single waterway.

Since the effective closure, the global fertiliser supply chain has contracted by 33%, according to real-time data from analytics firm Kpler and commodity analysis company CRU. The 22 million tonnes of urea the Gulf region exports annually have stalled. Roughly half of the 2.1 million tonnes of urea stockpiled over the past two years could not be loaded onto vessels due to logistical disruptions. Prices have responded: urea jumped from $482.5 per tonne on February 27 to $720 by mid-March, a near-50% increase in under three weeks. West Asian ammonia prices climbed 24%, approaching $600 per tonne. Fitch Ratings has since raised its 2026 ammonia and urea price expectations by around 25%, warning that a prolonged closure could push expectations higher still.

India’s Gas Problem Is Already India’s Food Problem

India sits close to the centre of this crisis, and the reasons are structural. The country runs its domestic urea plants on LNG imports from the Persian Gulf. When those flows stopped, so did production. Indian urea producers began shutting plants as LNG supply was cut, reported by Bloomberg in early March 2026, with ammonia import disruptions compounding the shortfall.

New Delhi’s response was to downgrade the fertiliser sector to a secondary priority in its natural gas allocation framework, capping industrial gas supply at the 70-75% range. That decision is what produced the 8,00,000-tonne monthly production gap. For a country with 1.4 billion people, a farming population that depends on subsidised urea, and a government that absorbs fertiliser costs through the subsidy regime, this is a direct fiscal and agricultural pressure that has already been set in motion.

Qatar’s state-owned fertiliser producer QAFCO, which runs a urea plant with an annual capacity of 5.6 million tonnes, has shut down over energy supply disruptions. Major production facilities in Bangladesh and Pakistan have halted completely. The Gulf is not a swing supplier that India can replace at whim.

A Crisis Worsened By Timing

The timing of the crisis makes the damage harder to contain. In the northern hemisphere, spring planting season is when nitrogen fertiliser application is most time-sensitive, with farmers typically ordering fertiliser in March to apply in April and May.

The Financial Times reported that winter wheat across the US, Europe, and parts of West Asia needs its final nitrogen application within a three-to-four-week window. In India, the overlap of rabi crop harvests with kharif sowing preparations means any input scarcity in this period translates directly into output decisions. Research from professors at the United Nations University, published in The Conversationnotes that even modest reductions in nitrogen application can produce disproportionately large yield declines, given how crops respond to nitrogen availability.

Globally, corn planting estimates are already being revised downward as farmers rotate towards soybeans, which do not require added nitrogen. That rotation locks in yield losses before a single seed enters the ground. The cost registers months later, at the level of food supply and retail price.

What India Can Do, And What It Should Have Done By Now

India is not without options, but none of them resolve quickly.

In the near term, India could accelerate LNG procurement from alternative suppliers, including the US and Australia, or through spot market purchases. That option is not a permanent solution, though. Australia sources over 60% of its urea from West Asia and expects current stocks to run out by mid-April. Rerouting supply chains through non-Gulf producers is possible in theory, but logistics costs are already elevated, and with 46% of global urea supply originating from the Gulf, that share cannot be replicated from elsewhere on a seasonal timeline.

The harder structural absence is a strategic fertiliser reserve. As the Financial Times noted, G7 countries do not maintain strategic fertiliser stockpiles to match their oil reserves, and no such reserve exists in India either. No emergency procurement authority clearly covers urea and ammonia the way strategic petroleum reserves Cover and Brent crude. What India can pursue immediately is bilateral procurement agreements with alternative suppliers and coordination with the FAO and WFP to monitor food price transmission before it reaches the retail level.

Furthermore, insurance premiums for vessels attempting to transit the strait have surged from 0.25% of a ship’s value to 10% for high-risk routes, according to Maximo Torero, chief economist at the UN Food and Agriculture Organization. Torero noted that even if hostilities end soon, insurers will reduce premiums only after a sustained period without new damage claims, which means maritime trade will take months to normalise regardless of military developments on the ground.

The costs India is bearing right now are the early-stage costs: reduced production, diverted gas allocation, and elevated import prices. The retail-stage costs, visible to the ordinary consumer at a kirana store or a wholesale market, are still weeks from arriving. Food price spikes above 30-40% have a documented correlation with political instability in fragile states within six to 18 months of the price trigger, per Financial Times analyses. India is not a fragile state, but with inflation already a political pressure point, the government cannot afford to treat an 8,00,000-tonne monthly production gap as a fluctuation it can wait out.

March 24, 2026, 7:03 PM IST

Read More

Source link

[ad_3]